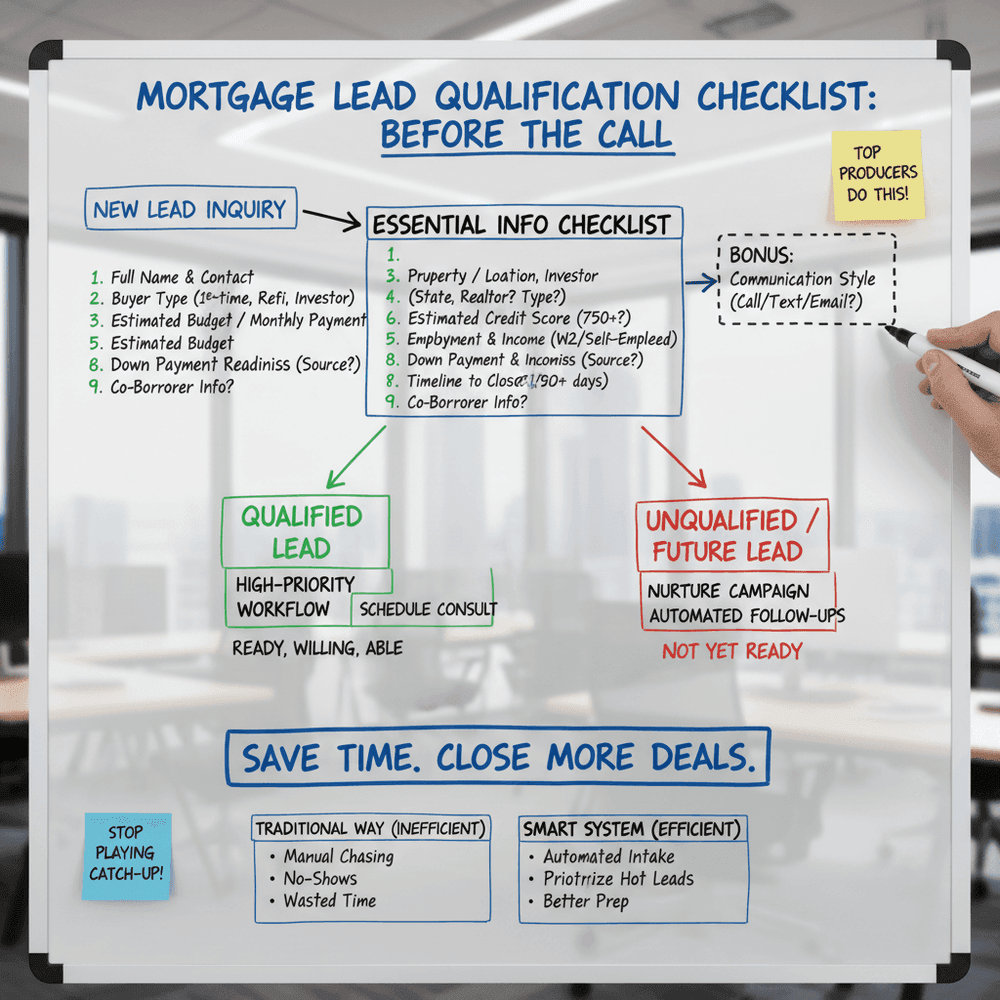

Mortgage Lead Qualification Checklist: What You MUST Know Before the First Call

So, you get a new lead. You're pumped — another potential homeowner, maybe even your next closed deal. But hold up — before you block out time for a discovery call or start calculating rates, let’s make sure your new lead is actually worth your time.

In an industry where minutes matter and unqualified leads eat up hours, it's critical to have a streamlined Mortgage Lead Qualification Checklist in place. Whether you’re a busy loan officer working nonstop or a brokerage juggling high-volume inbound activity, nailing down the right info early can save you tons of time and missed opportunities.

Let’s dive into the key details you need before you ever get on the phone. 👇

---

Why Mortgage Lead Qualification Matters More Than Ever

Here's a hard truth: not everyone who fills out a form or dials your number is serious — or even remotely prepared — to take the next step in home financing. In a market where demand fluctuates and interest rates are always shifting, knowing who's ready, willing, and able can make or break your monthly goals.

The more you can qualify upfront, the more productive your pipeline becomes. You book fewer no-show consults, waste less time repeating yourself, and start every conversation with clarity and purpose.

---

The Minimum Info You Need Before That First Consult

Start using this checklist as your lead filter. It’ll help ensure you're speaking only with serious prospects who are ready to move — not just “curious browsers.”

✅ 1. Full Name and Best Contact Info

Simple, but crucial. You’d be surprised how many leads go halfway through a form and skip this part. No contact info = no consult.

- Why it matters: For follow-up, cross-checking with CRM data, and prepping for the call.

- Bonus tip: Ask “What’s the best time to reach you?” to qualify their urgency.

---

✅ 2. Type of Buyer

Are they a first-time buyer, refinancing, real estate investor, or shopping for a second home?

- Why it matters: Every type of buyer has vastly different financing needs and expectations.

- What to ask: “What are your goals with this mortgage?” or offer a dropdown in your lead form.

---

✅ 3. Property Details or Desired Location

Whether they already have a property in mind or are just starting their search, know this:

- Are they buying in your licensed state(s)?

- Are they working with a realtor yet?

- What type of property are they after? (Condo, single-family, multi-unit?)

---

✅ 4. Estimated Budget or Price Range

This is where things get real. Ask upfront what their budget is — or at least get a ballpark figure.

- Why it matters: It tells you right away if their expectations align with today’s market.

- Insider tip: Asking for “monthly payment comfort zone” can feel less intimidating than asking for home price.

---

✅ 5. Estimated Credit Score

This scares some people off — but it shouldn't. Frame it as a way to help them, not judge them.

- “Would you say your credit is Excellent (750+), Good, Fair, or Needs Help?”

- Why you need it: Their range gives you a sense of what loan products to explore (or avoid).

---

✅ 6. Employment & Income Snapshot

Before locking in pre-approvals or discussing loan structures, confirm where the money’s coming from.

- Are they employed W2, self-employed, or somewhere in between?

- What’s their approximate annual income?

This helps identify what documentation you’ll need later — and if they’re even pre-qualification ready.

---

✅ 7. Down Payment Readiness

Few things open doors faster than a client who’s saved up. At minimum, ask:

- “How much are you planning to put down?”

- “Is this coming from savings, a gift, or other sources?”

No down payment isn’t necessarily a deal-breaker, but it helps set expectations early.

---

✅ 8. Timeline to Close

Is this lead planning a purchase in 30 days or 12 months?

- Urgent buyers should be moved into a high-priority workflow.

- Future buyers may benefit from nurture campaigns until they’re ready.

This one question helps massively with pipeline forecasting and time allocation.

---

✅ 9. Co-Borrower Info (if applicable)

No one likes surprises at underwriting. If they have a spouse or co-signer, ask up front.

- Do they have a co-borrower?

- Will both be on the loan?

---

Bonus: Qualify Based on Communication Style

Some clients love calling on the phone. Others shoot a text and vanish. If you can figure out their preferred communication style, your follow-ups will be a lot smoother.

Add a quick field or ask:

- “Do you prefer calls, texts, or emails?”

You’ll waste less time playing outreach ping-pong.

---

Where Most Mortgage Pros Miss the Mark

A lot of mortgage teams wait until the call to gather this info — or worse, try to piece it together after multiple conversations. That’s not just frustrating — it’s inefficient.

Imagine having all this info before you even say hello. You could:

- Prep better for every lead

- Prioritize hot prospects first

- Automate follow-ups based on their readiness level

That’s how top producers stay ahead without working 24/7.

---

Make Your Lead Intake Work Harder (So You Don’t Have To)

Let’s face it: manually chasing down all this info isn’t sustainable when leads come in at 5 p.m. on a Friday or when you're mid-closing. That’s where smart systems (and even smarter assistants 😉) can help you automate the front-end without losing the human touch.

Set up scripts, guide conversations, and qualify leads automatically, even when you’re busy on other calls.

Because qualifying leads shouldn’t feel like playing 20 Questions — and your nights and weekends weren’t meant for answering calls.

---

Final Thoughts: Stop Playing Catch-Up With Unqualified Leads

Great mortgage consults start with great prep. When you know who you’re talking to — and what they actually need — your conversion rate skyrockets, your time is better managed, and your stress? Way down.

Use this checklist as your qualification cheat sheet and start every conversation from a place of confidence and clarity. Whether you're scaling a growing team or solo-closing deals on the daily, this can be your new standard for smarter, faster mortgage consults.

---

TL;DR: Know your lead before the call. Get the essentials:

- Contact info

- Buyer type

- Property & budget details

- Credit & income snapshot

- Down payment and timeline

The rest? Let smart systems handle it.

👌 You’ve got deals to close — not calls to chase.

---